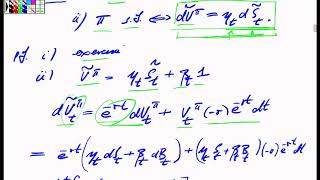

Media Summary: Black-Scholes Model: Completenes and Risk neutral Pricing, Hedging of Exotic Options: Up-and-Out-Call. Okay earlier we talked about a birth step burst this process there is a continuous time MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013 View the complete course: ...

Stochastic Processes Lecture 24 - Detailed Analysis & Overview

Black-Scholes Model: Completenes and Risk neutral Pricing, Hedging of Exotic Options: Up-and-Out-Call. Okay earlier we talked about a birth step burst this process there is a continuous time MIT 18.S096 Topics in Mathematics with Applications in Finance, Fall 2013 View the complete course: ... Markov Chains (I) First intuitive examples of Markov Chains 02:00 Definition of a Markov Chain 08:30 -- Note: The Set E_m in this ... MIT 18.642 Topics in Mathematics with Applications in Finance, Fall 2024 Instructor: Peter Kempthorne View the complete course: ... Brownian motion, construction via diffusive scaling of simple random walk: Tightness & Prokhorov theorem, Aldous criterion, ...

Invariant Measures, Prokhorov theorem, Bogoliubuv-Krylov criterion, Laypunov function approach to existence of invariant ...

![[Probability & Stochastic Processes] - Lecture 24: COUNTING PROCESSES](https://i.ytimg.com/vi/IdV2PyiJOv0/mqdefault.jpg)

![[Probability & Stochastic Processes] - Lecture 11: DISCRETE STOCHASTIC PROCESSES](https://i.ytimg.com/vi/1VruQ0HSgB8/mqdefault.jpg)